For families in our service areas

For families in our service areas, this guide explains caregiving and how non-medical in-home caregiving can support care planning in East Idaho, Treasure Valley & Magic Valley, Northern Wasatch, North Central West Virginia, and Northeast Ohio.

Why Open a Joint Bank Account with Your Matters

Navigating the financial landscape for elderly parents can often feel overwhelming. The challenge of managing shared resources, particularly through joint bank accounts, has become increasingly common. While these accounts allow families to collaborate on financial management, they also introduce complexities and potential pitfalls that can raise critical questions about trust and responsibility.

Families must consider how to strike the right balance between support and security when opening a joint bank account with an elderly parent. This arrangement can lead to misunderstandings and conflicts if not approached carefully. Therefore, it’s essential to understand the implications of such financial decisions and how they affect both parties involved.

To address these challenges, families should establish clear communication about financial expectations and responsibilities. Setting boundaries and discussing how funds will be used can help prevent disputes. Additionally, seeking advice from financial professionals can provide valuable insights into managing joint accounts effectively.

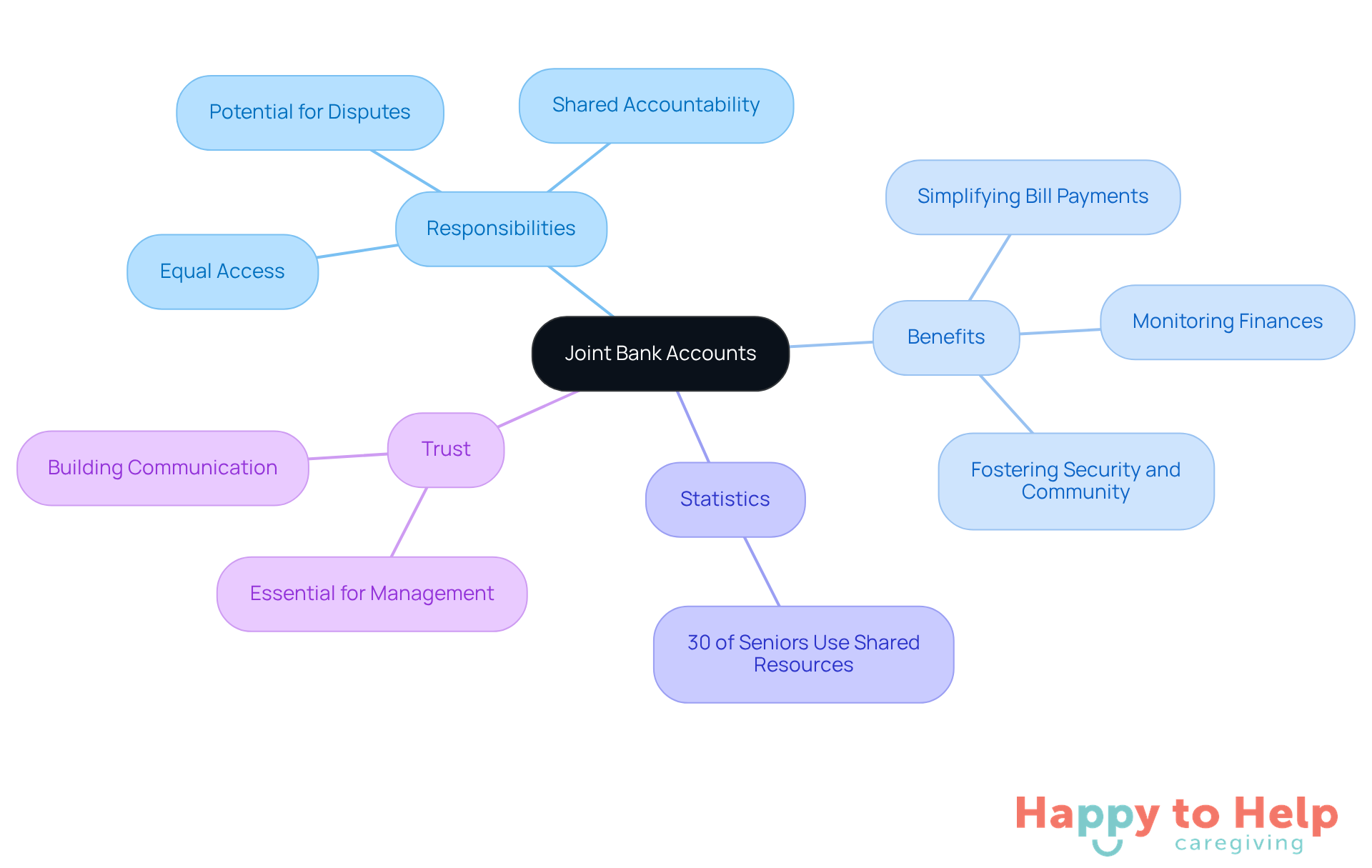

Understand the Basics of Joint Bank Accounts

A joint bank fund presents a challenge for many seniors, as it is a financial asset shared by two or more individuals, granting equal access to resources. While this arrangement allows each holder to deposit, withdraw, and manage funds independently, it also means that both parties share equal responsibility for any financial activity, including debts incurred. If one holder overspends or incurs fees, both are held accountable. Recent data shows that approximately 30% of seniors utilize shared financial resources, underscoring their popularity for collaborative financial management.

Understanding the terms and conditions set by financial institutions regarding shared finances is crucial, as these can vary significantly. For instance, some banks may require a minimum opening deposit, while others might impose specific rules on fund management. Real-life examples illustrate the benefits of a joint bank account with an elderly parent, such as simplifying bill payments and allowing adult children to monitor finances for unusual transactions, which can help reduce the risk of fraud.

Trust is essential when managing a shared fund, as all individuals have access to the resources. This arrangement, which may include a joint bank account with an elderly parent, can foster a sense of security and community, particularly for elderly parents who may need assistance with their finances. By pooling resources, families can enhance communication and ensure that monetary responsibilities are effectively shared.

Explore the Benefits of Joint Accounts for Seniors

Establishing a joint bank account with your elderly parent addresses a significant problem: managing finances effectively. Many elderly individuals face challenges in handling financial tasks due to age-related difficulties, which can lead to missed payments and financial mismanagement. For instance, the average monthly care costs can reach about $1,500, making it crucial to ensure that funds are allocated correctly and on time.

This situation can be further aggravated by the risk of fraud. Seniors are often targeted by scammers, and without proper oversight, unauthorized transactions can go unnoticed. Having a joint bank account with an elderly parent allows caregivers to monitor transactions closely, providing an essential layer of security for their parent’s finances.

In emergencies, having shared funds can be a lifesaver. Quick access to resources enables caregivers to respond swiftly to unexpected situations, such as urgent medical expenses or immediate care needs. This accessibility can make a significant difference in critical moments.

Moreover, shared funds simplify estate planning. Upon a parent's passing, the assets in the shared account automatically transfer to the surviving holder, bypassing the lengthy probate process. However, it’s vital to consider potential family disputes that may arise, as siblings might contest the distribution of funds. Additionally, shared resources can impact eligibility for aid programs like Medicaid, which is a crucial consideration for families managing elderly care.

Ultimately, while a joint bank account with an elderly parent can help streamline money management, it requires careful consideration of family dynamics and financial implications. Consulting with an investment advisor can provide tailored guidance to navigate these complexities effectively.

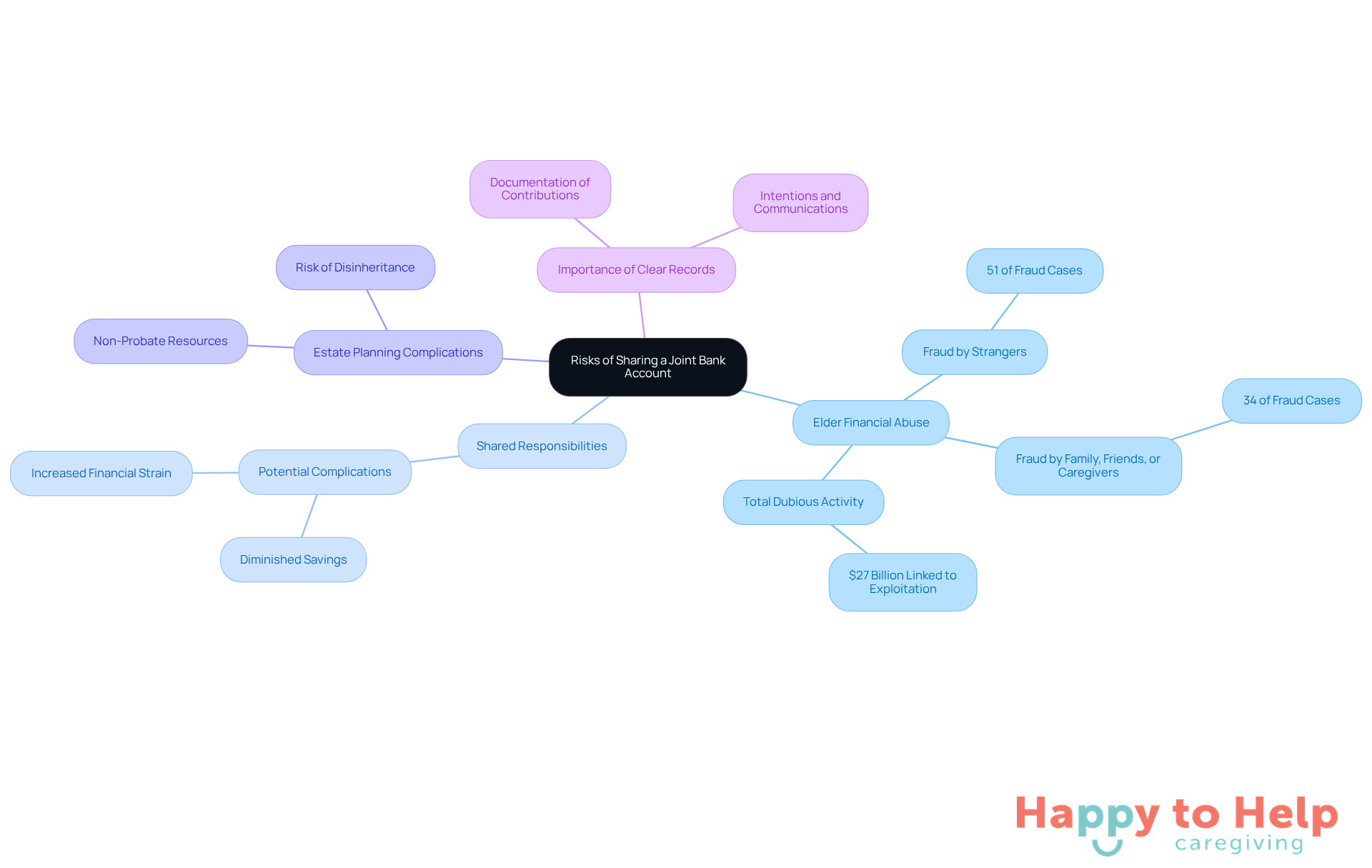

Identify the Risks of Sharing a Joint Bank Account

While a joint bank account with an elderly parent can streamline money management, it also presents notable dangers, particularly concerning elder financial abuse. This exploitation occurs when one shared holder misuses resources, jeopardizing the economic security of the other. Alarmingly, statistics show that about 51% of fraud against older adults is committed by strangers, while 34% is perpetrated by family, friends, or caregivers. This highlights the vulnerability of seniors in these situations. Furthermore, a FinCEN analysis revealed approximately $27 billion in dubious activity linked to elder exploitation over a one-year period ending in June 2023. This underscores the importance of vigilance when managing a joint bank account with elderly parent.

Both holders share responsibility for any debts or overdrafts, which can lead to complications if one party faces financial difficulties. This shared responsibility may result in unintended consequences, such as diminished savings or increased financial strain.

Joint holdings can also complicate estate planning. For instance, in Pennsylvania, funds in a shared account are generally considered non-probate resources that transfer directly to the surviving holder upon death. This can lead to assets being distributed against the deceased's wishes, potentially disinheriting other heirs. The remaining holder is under no obligation to share the assets, raising the risk of unintentional disinheritance. Legal disputes may arise, with heirs challenging the validity of the records or arguing that the account was intended only for convenience, gifts, or loans.

Given these complexities, it is crucial to maintain clear records of contributions, intentions, and communications related to the joint bank account with elderly parent. This practice can help prevent disputes and protect both parties' interests. Consulting with a legal expert can provide valuable insights into navigating these risks and ensuring that financial arrangements align with long-term goals.

Follow Steps to Open a Joint Bank Account

Opening a joint bank account with an elderly parent can be a crucial step in managing finances effectively. Caregivers often face challenges in ensuring that their loved ones have access to funds while maintaining oversight to prevent fraud. This situation can lead to stress and confusion, especially in emergencies when quick access to money is needed.

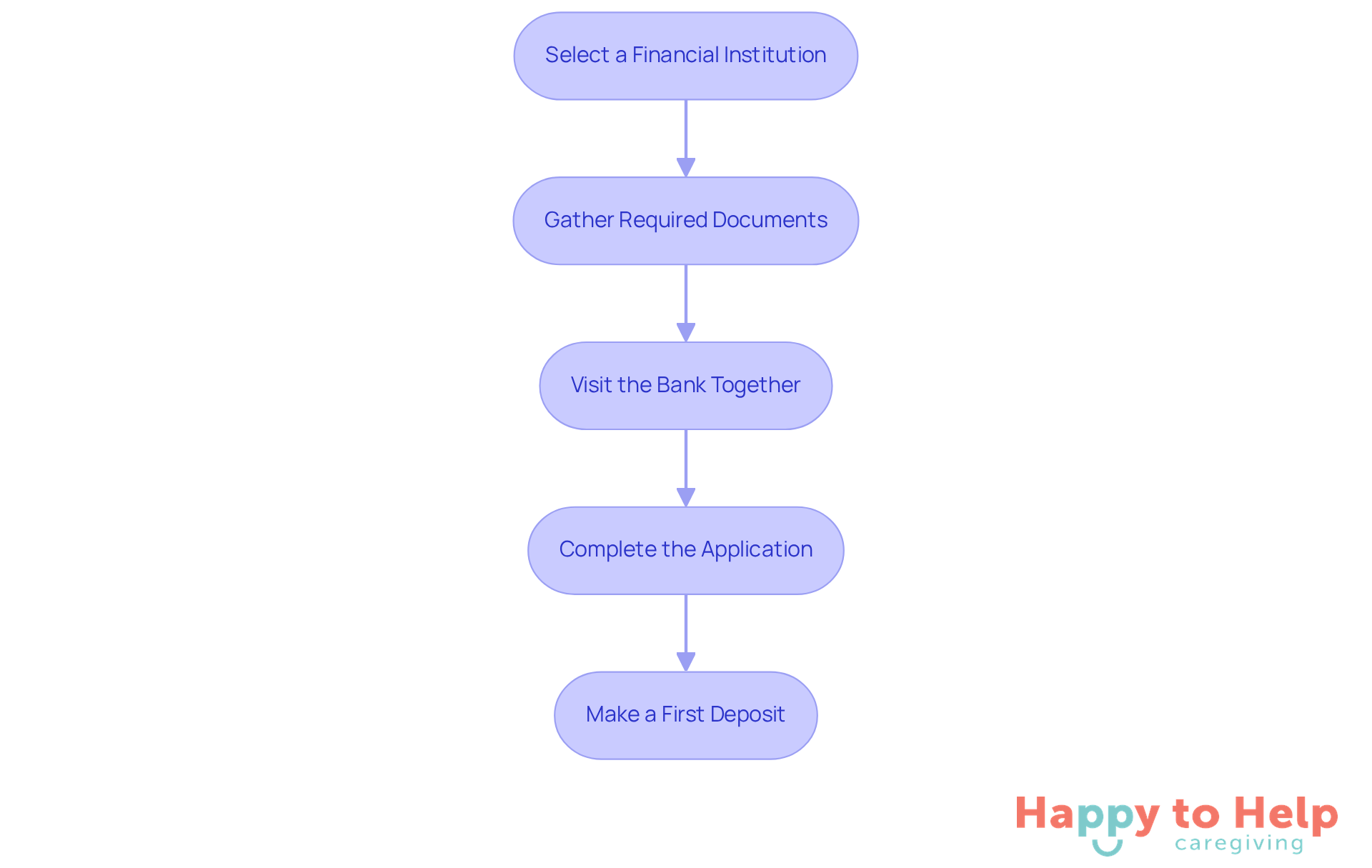

To address these concerns, here are essential steps to open a joint bank account:

- Select a Financial Institution: Investigate nearby financial organizations or credit unions that offer favorable conditions for joint accounts, such as low fees and excellent customer service.

- Gather Required Documents: Both parties will need identification, typically including a government-issued ID, Social Security numbers, and proof of address, like a utility bill or lease agreement.

- Visit the Bank Together: Both account holders must be present to open the account. Scheduling an appointment can help ensure a smooth process.

- Complete the Application: Fill out the application form provided by the financial institution, ensuring all information is accurate and matches the identification documents.

- Make a First Deposit: Be prepared to provide a first deposit, as some institutions require this to activate the account. The amount may vary, so check with the bank beforehand.

Creating a joint bank account with an elderly parent can enhance financial management and support for senior citizens. It allows caregivers to access funds in emergencies and monitor transactions to prevent fraud. Research shows that joint financial arrangements can help manage shared expenses, including housing costs and utility bills. Trust and clear communication between account holders are vital for a successful setup. As Hanna Horvath, a CFP and Bankrate Banking Editor, states, "A shared financial resource makes sense - and can simplify matters - for those that incur expenses together or have common savings objectives, such as a down payment on a home."

Typically, establishing a joint account takes about 30 minutes to an hour, depending on the institution's requirements.

Consider Alternatives to Joint Bank Accounts

If a joint bank account with an elderly parent doesn’t seem like the right fit, caregivers face a significant challenge in effectively managing their parent’s finances. The implications of this can be serious, especially when considering potential inheritance complications. A joint bank account with an elderly parent means that money is owned equally by both parties, allowing either to withdraw funds without the other’s consent, which can lead to disputes and financial mismanagement.

To navigate these challenges, consider the following alternatives:

- Power of Attorney: Designate a trusted individual to manage financial matters on behalf of your parent without sharing an account. This legal document allows the agent to conduct transactions, settle bills, and oversee assets, ensuring that your parent's monetary needs are addressed even if they become incapacitated.

- Convenience Funds: These arrangements enable an individual to access resources for specific purposes, such as settling bills, without providing complete ownership. This can simplify financial management while protecting the parent’s assets.

- Payable on Death (POD) Funds: This option allows resources to transfer directly to a beneficiary upon the holder's death, bypassing probate. It ensures that your parent’s assets are transferred smoothly and efficiently to the designated beneficiary.

- Authorized User Status: Instead of a shared account, you can be added as an authorized user on your parent's existing account. This status allows you to assist in managing finances without shared ownership, providing access to funds for essential expenses while preserving the parent's authority over the arrangement.

Consulting a certified financial advisor or elderly welfare expert can also guide families in making informed decisions regarding these financial management tools.

Taking the Next Steps

Establishing a joint bank account with an elderly parent presents a significant challenge for many caregivers. The problem lies in managing finances effectively while ensuring trust and communication. Without a clear financial arrangement, caregivers may struggle to monitor transactions, increasing the risk of fraud and complicating the sharing of financial responsibilities.

This situation can lead to serious implications, such as elder financial abuse and difficulties in estate planning. Caregivers need to be aware of these risks while also recognizing the benefits of joint accounts, which include improved oversight and emergency access to funds. However, alternatives like power of attorney and payable on death funds can also provide valuable options for families looking to manage finances without shared ownership.

To address these challenges, it’s crucial to approach the decision of opening a joint bank account with careful consideration. Engaging in open discussions with all parties involved and consulting with financial or legal professionals can help ensure that the chosen approach aligns with the long-term goals of both the elderly parent and their caregivers. By taking these steps, families can create a supportive financial environment that respects the autonomy of seniors while safeguarding their financial well-being.

https://iframe.tely.ai/cta/eyJhcnRpY2xlX2lkIjogIjY5Mjc5NTE5NmFmMzU5NTU2OTU3ODdkZSIsICJjb21wYW55X2lkIjogIjY4ZWU1ZGNhNzMxNzYyNTU3ZjNjOTVjMSIsICJpbmRleCI6IG51bGwsICJ0eXBlIjogImFydGljbGUifQ==Frequently Asked Questions

What is a joint bank account and how does it work?

A joint bank account is a financial asset shared by two or more individuals, allowing each holder to deposit, withdraw, and manage funds independently. However, all parties share equal responsibility for any financial activity, including debts incurred.

What are the benefits of having a joint bank account for seniors?

Joint bank accounts help seniors manage finances effectively, simplify bill payments, allow caregivers to monitor transactions for fraud, provide quick access to funds in emergencies, and streamline estate planning by automatically transferring assets upon a parent's passing.

What challenges might arise from a joint bank account?

Challenges include shared accountability for financial activities, potential family disputes over fund distribution after a parent's passing, and the impact on eligibility for aid programs like Medicaid.

Why is trust important when managing a joint bank account?

Trust is essential because all individuals have access to the shared resources. A trustworthy arrangement fosters a sense of security and community, particularly for elderly parents who may need assistance with their finances.

How can a joint bank account help prevent financial mismanagement among seniors?

A joint bank account allows caregivers to closely monitor transactions, helping to prevent missed payments and unauthorized transactions, which are common risks for seniors.

What should families consider before establishing a joint bank account?

Families should consider family dynamics, the potential for disputes over fund distribution, the impact on financial aid eligibility, and the specific terms and conditions set by financial institutions regarding shared finances. Consulting with an investment advisor can also provide tailored guidance.

List of Sources

- Understand the Basics of Joint Bank Accounts

- Legal Notes: Joint Bank Accounts—A Convenient Tool, with Pitfalls - LifePath (https://lifepathma.org/stories/legal-notes-joint-bank-accounts-a-convenient-tool-with-pitfalls)

- Nearly 1-in-4 married couples don't have a joint bank account, Census Bureau data shows — what's behind this trend (https://finance.yahoo.com/news/nearly-1-4-married-couples-103000307.html)

- Trends in Joint Bank Account Ownership Within Couples: 1996-2023 (https://census.gov/data/tables/2023/demo/wealth/joint-bank-act-ownship-w-couples.html)

- This Is How a Joint Bank Account Works (https://usnews.com/banking/articles/what-is-a-joint-bank-account)

- How Joint Bank Accounts Work, And How Sometimes, They Don’t – Law Firm of Daniel J. Reiter, Esq. (https://djrattorney.com/how-joint-bank-accounts-work-and-how-sometimes-they-dont)

- Explore the Benefits of Joint Accounts for Seniors

- Joint Bank Account with Senior Parents - Understanding the Pros and Cons (https://seniorhelpers.com/nc/charlotte/resources/blogs/is-a-joint-bank-account-with-elderly-parents-right-for-you)

- Is a Joint Bank Account With an Elderly Parent Right for You? (https://aplaceformom.com/caregiver-resources/articles/joint-bank-accounts)

- The Benefits of Sharing a Joint Bank Account With Your Parents (https://kiplinger.com/personal-finance/the-benefits-of-sharing-a-joint-bank-account-with-your-parents)

- Should I Open a Joint Bank Account With My Elderly Parent? - Experian (https://experian.com/blogs/ask-experian/should-i-open-joint-bank-account-with-my-elderly-parent)

- Yahoo fa parte della famiglia di brand Yahoo. (https://finance.yahoo.com/news/how-to-manage-financial-caregiving-for-an-aging-parent-140047469.html)

- Identify the Risks of Sharing a Joint Bank Account

- Agencies Issue Statement on Elder Financial Exploitation (https://occ.gov/news-issuances/news-releases/2024/nr-ia-2024-130.html)

- The Hidden Dangers of Joint Bank Accounts in Pennsylvania Estate Disputes (https://stark-stark.com/news/the-hidden-dangers-of-joint-bank-accounts-in-pennsylvania-estate-disputes)

- Why Seniors Should Be Wary of Joint Accounts | Evans Law Firm (https://evanslaw.com/why-seniors-should-be-wary-of-joint-accounts)

- Financial Capacity and Financial Exploitation of Older Adults: Research Findings, Policy Recommendations and Clinical Implications - PMC (https://pmc.ncbi.nlm.nih.gov/articles/PMC5463983)

- Agencies Issue Interagency Statement on Elder Financial Exploitation | FDIC.gov (https://fdic.gov/news/financial-institution-letters/2024/agencies-issue-interagency-statement-elder-financial)

- Follow Steps to Open a Joint Bank Account

- Joint Bank Accounts Make for Happier Couples - UCLA Anderson Review (https://anderson-review.ucla.edu/joint-bank-account)

- Almost a Quarter of Married Couples Didn’t Have Joint Accounts in 2023, Up From 15% in 1996 (https://census.gov/library/stories/2025/09/married-but-separate.html)

- How To Open a Joint Bank Account (https://pnc.com/insights/personal-finance/spend/how-to-open-joint-bank-account.html)

- What Is A Joint Bank Account? How It Works And Do You Need One | Bankrate (https://bankrate.com/banking/what-is-a-joint-bank-account)

- Consider Alternatives to Joint Bank Accounts

- Senator Dianne Feinstein giving up power of attorney is raising questions. Here's what it means. (https://cbsnews.com/news/dianne-feinstein-power-of-attorney-what-it-means)

- No Leaping — Some Alternatives to Joint Bank Accounts (https://blog.aarp.org/thinking-policy/no-leaping-some-alternatives-to-joint-bank-accounts)

- Is a Joint Bank Account With an Elderly Parent Right for You? (https://aplaceformom.com/caregiver-resources/articles/joint-bank-accounts)

- Almost a Quarter of Married Couples Didn’t Have Joint Accounts in 2023, Up From 15% in 1996 (https://census.gov/library/stories/2025/09/married-but-separate.html)

- Joint Bank Account with Senior Parents - Understanding the Pros and Cons (https://seniorhelpers.com/nc/charlotte/resources/blogs/is-a-joint-bank-account-with-elderly-parents-right-for-you)