For families in our service areas

For families in our service areas, this guide explains caregiving and how non-medical in-home caregiving can support care planning in East Idaho, Treasure Valley & Magic Valley, Northern Wasatch, North Central West Virginia, and Northeast Ohio.

Why Joint Accounts with Elderly Parents: Matters

Managing finances for elderly parents often feels like navigating a complex maze, where every decision carries significant implications. Caregivers face the challenge of ensuring their parents' financial needs are met while maintaining security and oversight.

Joint accounts are a popular solution, offering convenience and efficiency. However, these shared arrangements can also introduce serious risks, including potential financial abuse and complications in estate planning. Caregivers must consider how to balance accessibility with security in these financial partnerships.

To address these challenges, families can implement several strategies:

- Consider setting clear boundaries on account usage to prevent misuse.

- Regularly review account statements together to maintain transparency.

- Consult with a financial advisor to explore alternative options that provide oversight without compromising security.

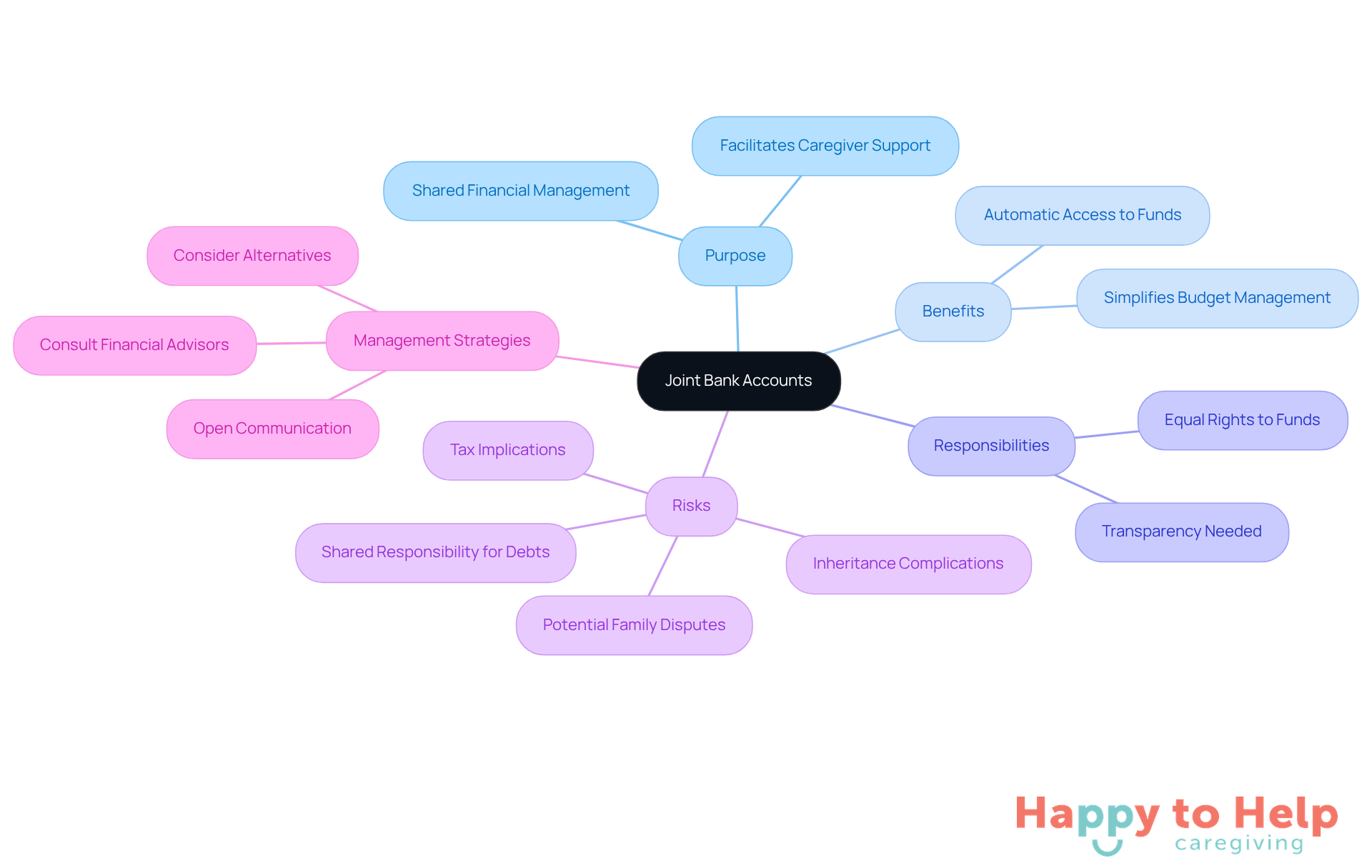

Define Joint Bank Accounts and Their Purpose

Managing finances for elderly parents can be challenging. Joint accounts with elderly parents, as a shared banking arrangement where two or more people pool their resources, can help alleviate some of these difficulties. This setup allows all holders to deposit, withdraw, and manage funds together, making joint accounts with elderly parents particularly beneficial for caregivers who assist them with financial matters.

However, while shared funds simplify budget management-enabling caregivers to pay for medical expenses or daily living costs-they also come with significant responsibilities. All holders have equal rights to the funds, which can lead to complications if transparency and trust are lacking. According to financial experts, shared funds can ease management but also expose both parties to risks, such as shared responsibility for debts and tax implications.

Statistics indicate that many older adults utilize shared resources, highlighting their popularity as a financial management tool. Yet, this trend comes with warnings from advisors about the importance of understanding the implications of shared access, especially concerning inheritance and financial security.

To effectively manage these arrangements, open communication among family members is crucial. Caregivers should discuss expectations and responsibilities upfront to mitigate risks. By doing so, joint accounts with elderly parents can act as a practical solution for managing finances, ensuring that the arrangement benefits everyone involved.

Explore Benefits of Joint Accounts for Elderly Care

The use of joint accounts with elderly parents offers significant benefits for elderly care, particularly in managing finances effectively.

Problem: Caregivers often struggle with the complexities of bill payments and financial oversight for their elderly parents. This can lead to stress and potential financial mismanagement.

Agitate: For instance, caregivers may find it challenging to ensure timely bill payments, risking late fees and added stress. Moreover, with over 88,000 fraud complaints reported in 2022, resulting in $3.1 billion in losses for victims aged 60 and above, the risk of economic abuse is a serious concern. The average loss per individual was $35,101, underscoring the need for vigilant oversight of shared funds.

The solution is that joint accounts with elderly parents simplify bill payments, allowing caregivers to manage and pay bills efficiently, thus minimizing the risk of late fees. This streamlined process alleviates stress, enabling caregivers to focus on providing support rather than navigating complex payment systems. Additionally, joint holdings enhance monetary oversight, allowing family members to monitor transactions closely and identify any unusual activities.

Convenience: With a joint account, caregivers can access funds directly without cumbersome legal processes, such as obtaining power of attorney for each transaction. This ease of access simplifies money management, making it easier to handle daily expenses and emergencies. However, having power of attorney paperwork on file can further clarify decision-making authority.

Emergency Access: In urgent situations, caregivers can quickly obtain funds to address unforeseen costs, ensuring peace of mind for both themselves and their aging parents. This immediate access is crucial for paying necessary bills, such as medical expenses, promptly, thereby avoiding potential disruptions in care.

In summary, managing joint accounts with elderly parents not only aids in managing resources but also enhances the quality of support provided to senior parents, ensuring their needs are met efficiently. However, caregivers should also consider the potential impact on Medicaid eligibility and inheritance issues that may arise from shared resources, as these factors can significantly influence long-term planning.

Identify Risks and Challenges of Joint Accounts

While joint accounts can offer convenience, they also pose significant risks that families must carefully consider:

-

Problem: Financial Abuse

Joint accounts can make elderly parents vulnerable to financial exploitation. Family members or caregivers may misuse the funds, leading to potential monetary abuse. AARP reports that nearly half of American adults have been victims or targets of financial exploitation, with family members identified as the most common perpetrators of elder abuse, according to the National Center on Elder Abuse. This emphasizes the necessity for vigilance in managing joint finances. -

Agitate: Loss of Control

All holders have equal access to the funds, which can lead to disputes or unauthorized withdrawals. This risk is especially noticeable if the aging parent has reduced capacity, making it challenging for them to oversee activity. -

Agitate: Impact on Medicaid Eligibility

Funds in a joint account are regarded as assets when assessing Medicaid eligibility. This can jeopardize an elderly parent's access to essential benefits, as even minimal funds may disqualify them from receiving assistance. For example, if a child is included in a parent's profile, it could impact the parent's eligibility for public benefits if the child becomes disabled. -

Agitate: Complicated Estate Issues

Upon the death of one holder, the funds in the shared account automatically transfer to the surviving holder. This can lead to disputes among heirs, particularly if other family members expected to inherit those funds. The legal presumption is that the surviving owner retains the balance, and they have no legal obligation to follow the deceased owner's estate plan, potentially resulting in unintentional disinheritance. -

Solution: Awareness and Vigilance

Comprehending these dangers is essential for families contemplating shared resources as a management strategy for aging parents. By being aware of the potential for monetary abuse, the implications for Medicaid eligibility, and the complexities surrounding estate management, families can make informed decisions that protect their loved ones' economic well-being.

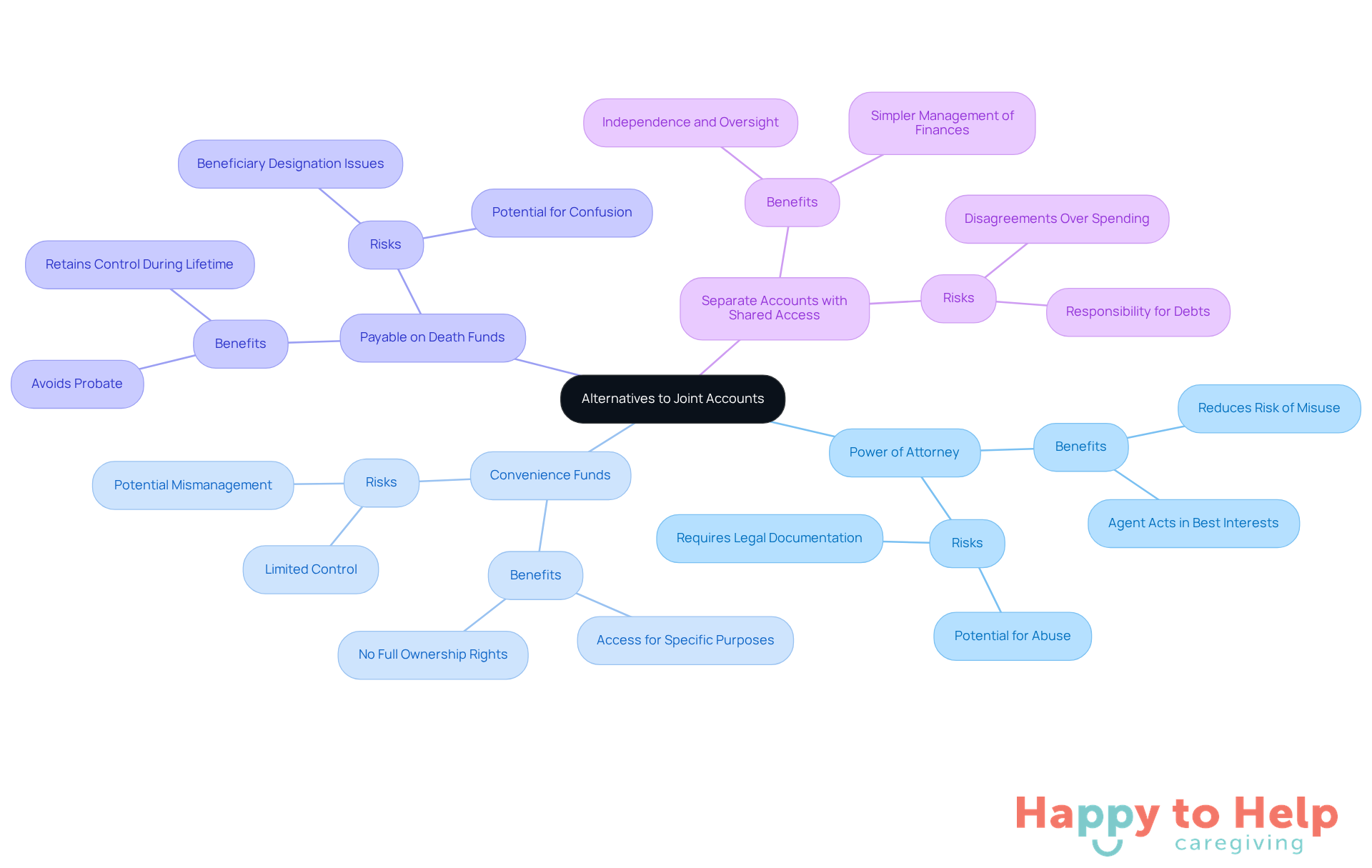

Consider Alternatives to Joint Accounts

Managing finances for elderly parents can be challenging, especially when considering the risks associated with joint accounts with elderly parents. These accounts can lead to potential elder abuse and complicate family dynamics, making it crucial to explore safer alternatives.

Here are several options that may better suit the financial management needs of elderly parents:

-

Power of Attorney (POA): Designating a trusted individual as a power of attorney allows them to manage financial matters without sharing account ownership. This arrangement significantly reduces the risk of misuse, as the agent is legally bound to act in the principal's best interests. According to AARP, 26 percent of monetary caregivers utilize joint resources for managing funds, highlighting the importance of understanding alternatives like POA.

-

Convenience Funds: These arrangements allow a designated individual to access resources for specific purposes, such as settling bills, without granting full ownership rights. This configuration can assist in optimizing financial tasks while safeguarding the holder's assets.

-

Payable on Death (POD) Funds: POD funds enable the holder to designate beneficiaries who will obtain the resources upon their passing. This method avoids probate and ensures that the holder retains control over their assets during their lifetime.

-

Separate Accounts with Shared Access: Maintaining separate accounts while linking them for shared expenses strikes a balance between independence and oversight. This method enables simpler management of finances without the risks linked to shared ownership, such as possible disagreements over spending or responsibility for debts.

It's essential to consider the emotional and legal implications of these financial decisions, as they can significantly impact family dynamics. These alternatives provide flexibility and security, ensuring that elderly parents can manage their finances effectively while minimizing risks associated with joint accounts with elderly parents.

Making the Right Choice

Managing finances through joint accounts with elderly parents can be a double-edged sword. While these shared banking arrangements simplify financial management, they also introduce significant risks that families must navigate carefully. The responsibility of shared access can lead to complications, particularly when trust and transparency are not prioritized.

The benefits of joint accounts are clear:

- Streamlined bill payments

- Immediate access to funds in emergencies

- Enhanced oversight of transactions

However, these advantages come with potential pitfalls, such as:

- Financial exploitation

- Impacts on Medicaid eligibility

- Complex estate issues that may arise upon a holder's death

Understanding these dynamics is crucial for families as they weigh their options.

To mitigate these risks, families should approach the decision to utilize joint accounts with caution. Exploring alternatives like power of attorney or separate accounts with shared access can provide safer solutions while still addressing the financial management needs of elderly parents. Engaging in open discussions and seeking professional advice are essential steps to ensure that financial arrangements protect the interests of all parties involved.

https://iframe.tely.ai/cta/eyJhcnRpY2xlX2lkIjogIjY5MjY2NjE2YmM0ODhkNDFmZWVlZWU0NCIsICJjb21wYW55X2lkIjogIjY4ZWU1ZGNhNzMxNzYyNTU3ZjNjOTVjMSIsICJpbmRleCI6IG51bGwsICJ0eXBlIjogImFydGljbGUifQ==Frequently Asked Questions

What are joint bank accounts and what is their purpose?

Joint bank accounts are shared banking arrangements where two or more people pool their resources, allowing all holders to deposit, withdraw, and manage funds together. They are particularly beneficial for caregivers managing finances for elderly parents.

How do joint accounts help caregivers of elderly parents?

Joint accounts simplify budget management for caregivers, enabling them to pay for medical expenses and daily living costs more easily.

What are the responsibilities associated with joint bank accounts?

All holders of a joint account have equal rights to the funds, which can lead to complications if there is a lack of transparency and trust. Additionally, shared funds expose both parties to risks such as shared responsibility for debts and potential tax implications.

Are joint accounts common among older adults?

Yes, statistics indicate that many older adults utilize joint accounts as a financial management tool, highlighting their popularity.

What should families consider before opening a joint account?

Families should understand the implications of shared access, especially regarding inheritance and financial security. Open communication about expectations and responsibilities among family members is crucial to mitigate risks.

How can families ensure that joint accounts benefit everyone involved?

By discussing expectations and responsibilities upfront, families can effectively manage joint accounts, ensuring that the arrangement serves the interests of all parties involved.

List of Sources

- Define Joint Bank Accounts and Their Purpose

- Joint Bank Account with Senior Parents - Understanding the Pros and Cons (https://seniorhelpers.com/nc/charlotte/resources/blogs/is-a-joint-bank-account-with-elderly-parents-right-for-you)

- ABA Foundation and AARP: What You Need to Know about Joint Bank Accounts (https://sdba.memberclicks.net/?option=com\_dailyplanetblog&view=entry&year=2015&month=08&day=27&id=20:aba-foundation-and-aarp-what-you-need-to-know-about-joint-bank-accounts)

- Is a Joint Bank Account With an Elderly Parent Right for You? (https://aplaceformom.com/caregiver-resources/articles/joint-bank-accounts)

- This Is How a Joint Bank Account Works (https://usnews.com/banking/articles/what-is-a-joint-bank-account)

- Should I Open a Joint Bank Account With My Elderly Parent? - Experian (https://experian.com/blogs/ask-experian/should-i-open-joint-bank-account-with-my-elderly-parent)

- Explore Benefits of Joint Accounts for Elderly Care

- Joint Bank Account with Senior Parents - Understanding the Pros and Cons (https://seniorhelpers.com/nc/charlotte/resources/blogs/is-a-joint-bank-account-with-elderly-parents-right-for-you)

- The Benefits of Sharing a Joint Bank Account With Your Parents (https://kiplinger.com/personal-finance/the-benefits-of-sharing-a-joint-bank-account-with-your-parents)

- Is a Joint Bank Account With an Elderly Parent Right for You? (https://aplaceformom.com/caregiver-resources/articles/joint-bank-accounts)

- Should I Open a Joint Bank Account With My Elderly Parent? - Experian (https://experian.com/blogs/ask-experian/should-i-open-joint-bank-account-with-my-elderly-parent)

- Why Seniors Should Be Wary of Joint Accounts | Evans Law Firm (https://evanslaw.com/why-seniors-should-be-wary-of-joint-accounts)

- Identify Risks and Challenges of Joint Accounts

- AARP Report Finds Nearly Half of U.S. Adults Targeted for Financial Exploitation (https://press.aarp.org/6-13-2024-AARP-Report-Nearly-Half-U-S-Adults-Targeted-Financial-Exploitation)

- Top 5 Reasons that Seniors Should Avoid Sharing a Joint Bank Account with an Adult Child - Cranfill Sumner LLP (https://cshlaw.com/resources/top-5-reasons-that-seniors-should-avoid-sharing-a-joint-bank-account-with-an-adult-child)

- Elder Abuse Statistics - Statistics on Elderly Abuse Over Time (https://nursinghomeabusecenter.com/elder-abuse/statistics)

- Tax and Wealth Advisor Alert: How Joint Accounts Can Ruin Your Estate Plan (https://wilaw.com/tax-wealth-advisor-alert-how-joint-accounts-can-ruin-your-estate-plan)

- How Joint Bank Accounts Affect Medicaid Eligibility (https://agingcare.com/articles/joint-bank-accounts-affect-medicaid-168094.htm)

- Consider Alternatives to Joint Accounts

- No Leaping — Some Alternatives to Joint Bank Accounts (https://blog.aarp.org/thinking-policy/no-leaping-some-alternatives-to-joint-bank-accounts)

- Joint Accounts with Adult Children: What Women Need to Know (https://savantwealth.com/savant-views-news/article/joint-accounts-with-adult-children-what-women-need-to-know)

- Elder Abuse Statistics - Statistics on Elderly Abuse Over Time (https://nursinghomeabusecenter.com/elder-abuse/statistics)

- Why a Power of Attorney is a Better Choice than a Joint Bank Account for Non-Spouses - Jamie Miller Law | Tulsa Business Lawyer (https://jmillerlawfirmpllc.com/why-a-power-of-attorney-is-a-better-choice-than-a-joint-bank-account-for-non-spouses)

- Powers of Attorney or Joint Accounts: What is the Best Way to Assist a Loved One with Finances? - McAndrews Law Firm (https://mcandrewslaw.com/publications-and-presentations/articles/powers-of-attorney-or-joint-accounts-what-is-the-best-way-to-assist-a-loved-one-with-finances)